Navigating 2026: Top Questions on ISG’s 2026 Outlook Answered

Q: How does the appointment of a new Fed Chair and the recent Supreme Court ruling on tariffs impact ISG's Outlook?

A: If confirmed by the Senate, Kevin Warsh will become Chair of the Federal Reserve. Warsh generally held hawkish views when he was a Fed Governor from 2006 to 2011, but more recently he has supported lower interest rates. ISG does not expect major changes to monetary policy if Warsh is confirmed as the new chair. Changes to the policy rate or the Fed’s balance sheet require a majority of the 12-person Federal Open Market Committee (FOMC) voting committee. If views diverge on the FOMC, more voting dissents are likely. Warsh has also indicated support for Fed reform, which could lead to changes in Fed communications and staffing. Periods of short-term volatility are possible as a result.

More broadly, an overly accommodative policy stance would likely prove self-defeating. Heightened inflation concerns would push long-term yields higher—an outcome outside the Federal Reserve’s direct control—and would thereby tighten financial conditions rather than easing them. In this way, the market itself can serve as the ultimate restraint on inappropriate policy.

On tariffs, ISG anticipates only a modest decline in the effective tariff rate from the Supreme Court's ruling against levies imposed under the International Emergency Economic Powers Act (IEEPA). The White House likely has the ability to reimpose tariffs under other authorities. The potential for refunds is uncertain, and even if required, the implications for the federal deficit and GDP growth would be modest.

Q: Are recent developments in the private credit market regarding Blue Owl's asset sale reflective of a systemic risk to the asset class or the banking system?

A: Headlines related to the Blue Owl asset sale and subsequent halt of fund redemptions in a private Business Development Company (BDC) have caused concerns around private credit, with alternative asset manager stocks selling off in recent weeks. Although this highlights a liquidity mismatch between investors looking for redemptions from their investments and an inherently illiquid asset class in private credit, it has added fuel to fears that private credit could be the next subprime. While these concerns are understandable, ISG believes that linkage between private credit stress and the broader banking system remains limited. Banks’ lending to private credit accounts for just ~4.2% of their total exposure to non-bank financial institutions (NBFIs).1

Individual investors make up just ~$200 billion of the private credit industry’s net asset values. Assuming a 20% annual redemption rate (5% max per quarter), the industry would face ~$40 billion of redemption requests—compared to ~$400 billion of available institutional capital sitting on the sideline across Direct Lending and Opportunistic Credit funds. As happened with Owl's recent loan sales, institutional investors could step in to raise needed liquidity.

On the whole, ISG does not believe that today’s leverage backdrop resembles the conditions that preceded past systemic credit events. In short, it seems more likely that private credit losses are idiosyncratic and investment-manager specific, rather than a signal of the next systemic credit event. ISG will continue to closely monitor the private credit market and keep clients informed if developments change this assessment.

Q: How much of a risk is the K-shaped economy?

A: The current K-shaped economy—where high-income households are experiencing stronger income growth than low-income households—bears watching but is not a material risk in ISG’s forecast. Consumption, which represents about 70% of GDP, continues to grow at a solid 2.5% annualized pace. While real income growth is weakest in the lowest quintile, it remains positive for all income cohorts. Importantly, middle- and top-income households, who account for a disproportionate share of total consumption, continue to see solid growth. Healthy household balance sheets have also allowed consumers to draw down savings to smooth their consumption. Net worth as a share of GDP is close to its decade-long trend and household debt relative to GDP is continuing a multi-year deleveraging cycle.

ISG’s base-case expectation is that inflation eases and the labor market modestly improves this year, which should support rising real incomes, and ultimately consumption, in 2026.

Q: What are ISG’s views on gold?

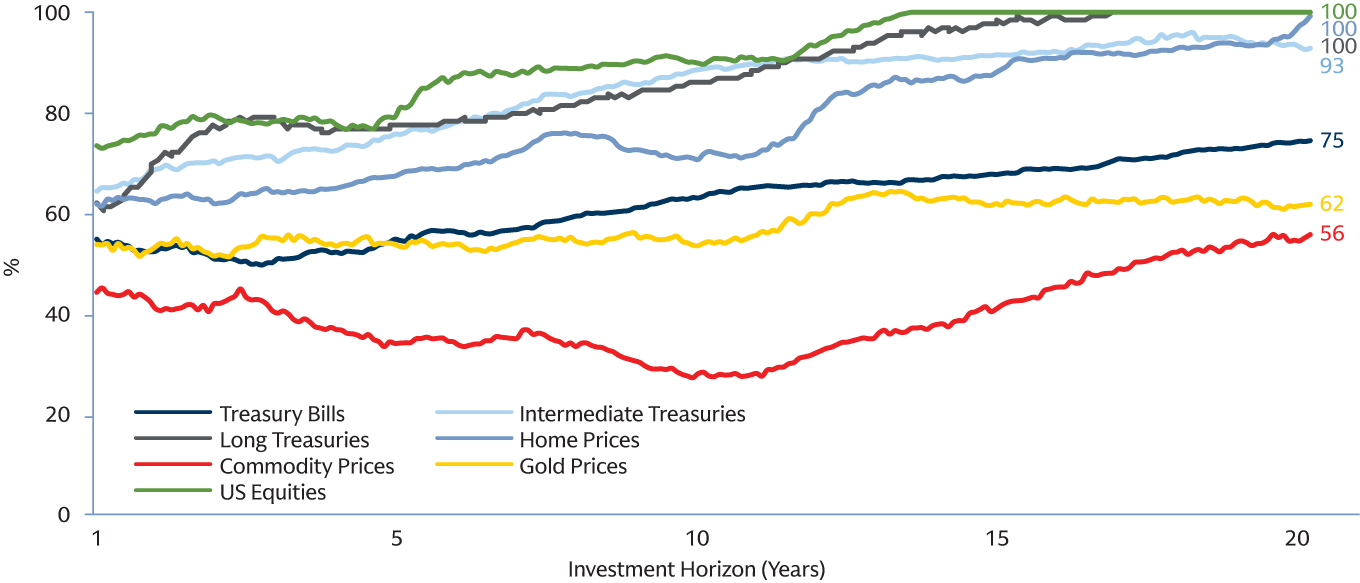

A: In assessing the case for a strategic allocation to gold, it is important to consider the reasons for adding an asset to a well-diversified portfolio: income generation, upside exposure to growth, hedging against inflation or deflation, or protection against downside risks. Historically, gold has not consistently satisfied these criteria. While gold is often considered an effective inflation hedge, the chart below highlights that the S&P 500 has more consistently fulfilled that role than gold, historically.

From a tactical perspective, ISG does expect gold prices to continue trending higher this year due to several factors—including persistent demand from central banks and investors. However, due to the recent sharp increase in gold prices and the high cost of implementation via options, ISG does not currently believe clients should add a tactical tilt to gold.

Q: What are the key risks to the 2026 Outlook?

A: ISG continually assesses the risks to its Outlook. Three variants of those risks include:

- Economic Risks: ISG has lowered its one-year recession probability to 25%. This stands above the 13% unconditional odds of recession since 1980, reflecting lingering risks from a still soft labor market. While this probability is elevated relative to history, it remains far from a base case.

- Geopolitical Risks: Investors continue to face a long list of geopolitical risks that can send jitters through financial markets. The key question is whether these risks could derail the US or global economies; ISG believes most will be contained and unlikely to alter their economic or market outlook. The only serious risk to ISG’s view would be a significant deterioration in US-China relations.

- Financial Market Drawdown Risks: ISG’s view to stay invested in US equities does not preclude occasional market pullbacks, which can happen at any time. Declines of 5–10% reflect typical volatility rather than a reason to underweight stocks. While elevated valuations mean there’s an 80%+ chance of a 10% pullback in any calendar year, the probability that such a decline persists through year‑end is only about 20%, indicating most pullbacks recover. As seen in recent years, those pullbacks can also occur after the market has first rallied significantly.

For more on geopolitical and US political risks, listen in to ISG’s recent webinar.

If you have questions about how the perspectives shared in this market update impact your financial portfolio, connect with your Goldman Sachs team.

1 Data through Q4 2024. Source: Investment Strategy Group, Board of Governors of the Federal Reserve System, Berrospide, Jose, Fang Cai, Siddhartha Lewis-Hayre, and Filip Zikes (2025). "Bank Lending to Private Credit: Size, Characteristics, and Financial Stability Implications," FEDS Notes. Washington: Board of Governors of the Federal Reserve System, May 23, 2025, https://doi.org/10.17016/2380-7172.3802.

This material is intended for educational purposes only and is provided solely on the basis that it will not constitute investment advice and will not form a primary basis for any personal or plan’s investment decisions. While it is based on information believed to be reliable, no warranty is given as to its accuracy or completeness and it should not be relied upon as such. Information and opinions provided herein are as of the date of this material only and are subject to change without notice. Goldman Sachs is not a fiduciary with respect to any person or plan by reason of providing the material herein. Information and opinions expressed by individuals other than Goldman Sachs employees do not necessarily reflect the view of Goldman Sachs. Information and opinions are as of the date of the event and are subject to change without notice.

The views expressed in this piece are those of the Investment Strategy Group (“ISG”), part of the Asset & Wealth Management business of Goldman Sachs, which focuses on asset allocation strategy formation and market analysis for Goldman Sachs Wealth Management and do not necessarily represent those of Goldman Sachs. Goldman Sachs Wealth Services is not providing any financial, economic, legal, accounting, or tax advice or recommendations in this video document. Opinions expressed are current opinions only.

ISG/GIR Forecasts. Economic and market forecasts presented (“forecasts”) reflect either ISG’s or Goldman Sachs Global Investment Research’s (“GIR”) views and are subject to change without notice. Forecasts do not consider specific investment objectives, restrictions, tax and financial situation or other needs of any specific client. Forecasts are subject to high levels of uncertainty that may affect actual performance and should be viewed as merely representative of a broad range of possible outcomes. Forecasts and any return expectations are as of the date of this material and should not be taken as an indication or projection of returns of any given investment or strategy. Forecasts are estimated, based on capital market assumptions, and are subject to significant revision and may change materially as economic and market conditions change. Any case studies and examples are for illustrative purposes only. If applicable, a copy of the GIR Report used for GIR forecasts is available upon request. Forecasts do not reflect advisory fees, transaction costs, and other expenses a client would have paid, which would reduce return.

The information contained herein is intended for informational purposes only, is not a recommendation to buy or sell any securities and should not be considered investment advice. The material is based upon information which we consider reliable, but we do not represent that such information is accurate or complete, and it should not be relied upon as such.

©2026 Goldman Sachs. All rights reserved.

Goldman Sachs & Co. LLC is registered with the Securities and Exchange Commission (“SEC”) as both a broker-dealer and an investment adviser and is a member of the Financial Industry Regulatory Authority (“FINRA”) and the Securities Investor Protection Corporation (“SIPC”).