Your Annual Gifting Strategy: Comparing Crummey Trusts, UTMAs, 529s, and Trump Accounts

- Trump Accounts can be established and funded beginning July 4, 2026.Children with a Social Security number who are under 18 are eligible for an account. Those born between 1/1/25 and 12/31/28 can receive a one-time, $1,000 contribution.

- The IRS has provided guidance on gift tax implications of Trump Account contributions.IRS Rev. Proc. 2026-25 provides a safe harbor rule that eliminates the gift tax return filing requirement for gifts to a Trump Account if certain conditions are met. Review with your tax and legal advisors.

- Trump Accounts differ from Crummey Trusts, UTMAs, and 529 plans.The differences span control, flexibility, and tax implications.

- Before taking action, work with a professional to understand how different gifting vehicles could impact wealth planning.Prioritizing gifting goals (e.g., retirement or education savings) can help pinpoint the most impactful options.

Laying a strong foundation for loved ones’ futures requires comprehensive and forward-thinking planning. There are a number of vehicles—including Crummey Trusts, UTMAs, 529 Plans, and now Trump Accounts—that can contribute to a family’s overall giving strategy, each with distinct purposes and characteristics that could have short- and long-term impact.

What is a Trump Account?

At its core, a Trump Account (TA) is a retirement savings vehicle for children.

A TA allows loved ones to support a child’s future by making financial contributions that will be invested and can compound over time. Funds cannot be accessed during this “growth period” by contributors or the child.

The growth period ends the calendar year the child turns 18, and the TA becomes subject to most traditional individual retirement account (IRA) rules (e.g., early withdrawal penalties and taxation rules). The child becomes the owner of the account and has full control over the funds within. They may choose to convert the TA to a traditional IRA at this time.

Do Trump Accounts Qualify for the Annual Gift Tax Exclusion?

As you evaluate the role of Trump Accounts (TAs) within your family’s long-term wealth strategy, consider the following structural characteristics:

- Gift tax considerations. IRS Rev. Proc. 2026-25 provides a safe harbor rule that eliminates the gift tax return filing requirement for gifts to a Trump Account if certain conditions are met. Review with your tax and legal advisors.

- Tax-deferred growth. Contributions and related investment earnings compound within the TA without being subject to income and capital gains taxes.

- Equity exposure. TA funds must be invested in a standard US stock market index fund like the S&P 500. This type of investment can provide long-term benefit and growth, though may also be subject to greater volatility and risk in the nearer term.

- Conversion to IRA. When the beneficiary turns 18, the TA becomes subject to most traditional IRA rules. The account can be rolled into a traditional IRA at this point, which would make it subject to all IRA rules.

- Encouraging long-term thinking early—with trade-offs to consider. TAs could provide financial education opportunities, given their restricted access (long-term planning) and retirement planning focus. However, with ownership transferring to the beneficiary at age 18, the parent or guardian loses oversight or control of the funds and decisions about next steps (e.g., taking early withdrawals). If more control is desired, alternative vehicles could be a better option.

- Philanthropic potential. Some philanthropists are looking at TAs as a new avenue for effecting change. Philanthropists can set parameters for their gifts, focusing on specific locations or school districts, supporting certain groups (e.g., families of veterans), or incentivizing participation in financial literacy programs.

- State-specific considerations. There may be state-level nuances to be aware of. Consult your tax and legal advisors to review your circumstances.

- PHILANTHROPY THROUGH TRUMP ACCOUNTSIn order to provide seed funding for children who don’t qualify for the federal government’s $1,000 contribution, Michael and Susan Dell pledged to donate $6.25 billion. The Dells committed to providing $250 to the TAs of children under 10 who 1) were born before the cutoff for the federal contribution, and 2) live in areas where the median income is less than $150,000.

Source: https://investamerica.org/

This is an illustrative example, not indicative of typical outcomes or strategies, and should not be interpreted as an endorsement of a strategy or product by Goldman Sachs.

Comparing Vehicles for Annual Gifting Strategies

Effectively utilizing the annual gift tax exclusion and (where applicable) the annual Generation Skipping Transfer (GST) tax exclusion—which covers gifts made to “skip persons” (e.g., grandchildren)—while preserving the lifetime exemption requires careful and proactive planning.

Given the nature of Trump Accounts, they have become part of the conversation in 2026, with many questioning how they could fit into an overall gifting strategy alongside Crummey Trusts, UTMAs, and 529 plans.

As you review your options for gifting, there are a few key planning points to keep top of mind and potentially discuss with your tax advisor.

Questions to ask when considering different gifting vehicles

- What is your primary objective for the gift?

- Who can control how the funds are invested?

- Who can control the distributions and to what extent?

- Are you able to regain access to the funds after the transfer?

- Is there flexibility in case of changed circumstances?

- What income, gift, estate, and GST tax benefits and liabilities are there?

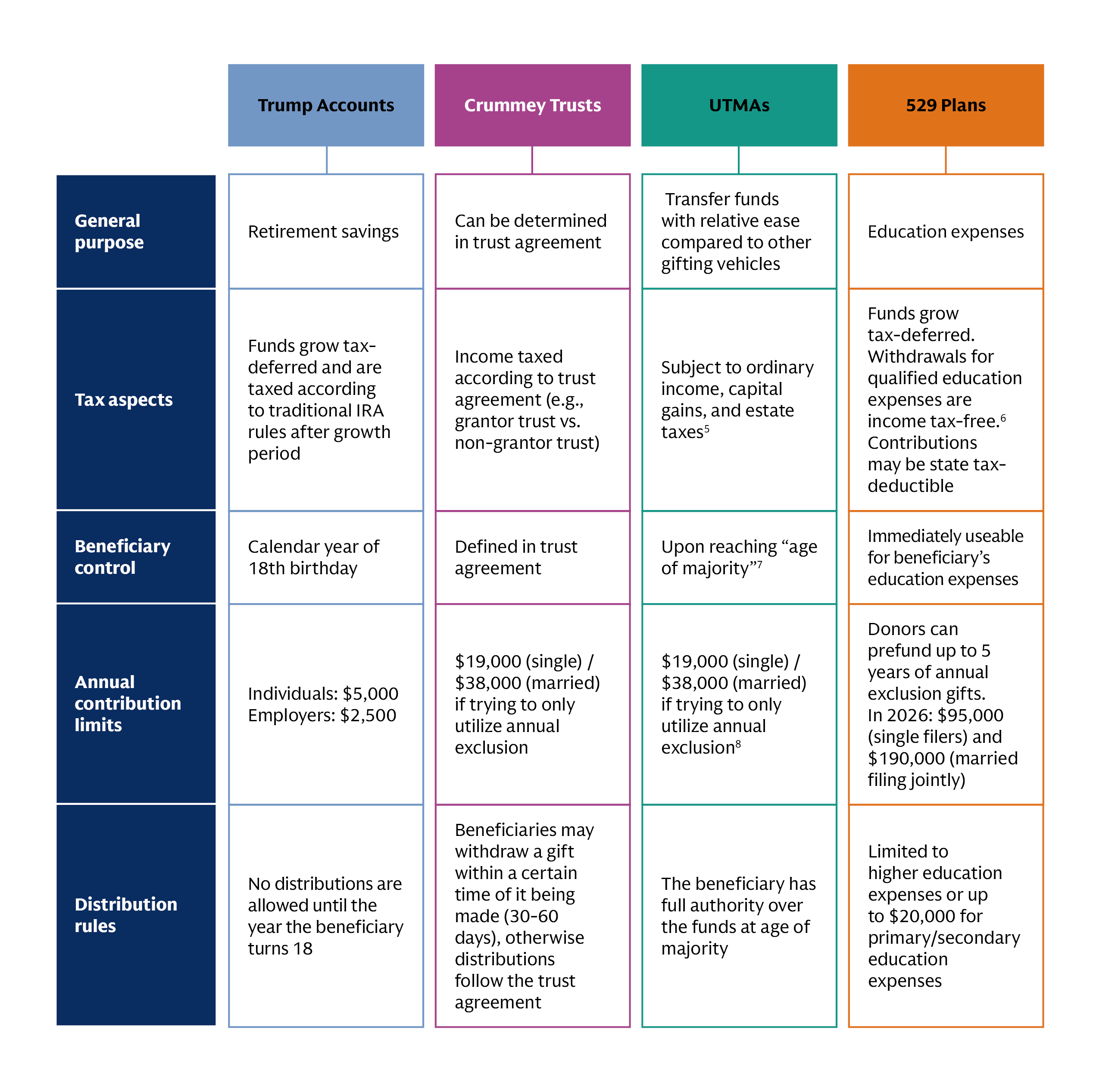

How Do Trump Accounts Compare to Common Gifting Vehicles?

While this article compares Trump Accounts, Crummey Trusts, UTMAs, and 529 plans, this is not an exhaustive list of options.2 Discuss specifics of each vehicle and how they could align with or impact plans you have in place with your wealth advisor.

Basic vehicle structure

- Trump Account: A new tax-advantaged retirement savings account for children.

- Crummey Trust: A type of irrevocable trust that allows the beneficiary to withdraw a gift within a certain amount of time of it being made (e.g., 30–60 days). Assets not withdrawn remain in the trust, to be distributed to beneficiaries according to the terms of the trust agreement.

- Uniform Transfer to Minors Act (UTMA) account: A custodial account holding assets legally owned by the minor but managed by a custodian—usually a parent—until the minor reaches the “age of majority” as defined by the state (i.e., 18, 21, or 25).

- 529 Plan: A tax-advantaged savings account used for qualified education expenses.

What is your primary objective for the gift?

As you consider which vehicles to include in your gifting strategy, think about the individuals you are providing for and your priorities for them. Specific-purpose vehicles will have limited applicability, but could provide unique benefits if they align with your goals for your loved ones.

- Trump Account: Long-term retirement savings

- Crummey Trust: No vehicle-specific purpose—this can be determined in the trust agreement

- UTMA: No vehicle-specific purpose but UTMAs offer relatively easy establishment and administration compared to other vehicles

- 529 Plan: Education expenses

Who can control how the funds are invested?

The amount of control needed can depend on personal preferences and circumstances. In cases where a vehicle provides less control over the investments within, some families elect to establish another vehicle that balances out the risks associated, gaining a level of control.

- Trump Account: TAs have specific rules around “eligible investments” (e.g., invested in a standard US stock market index fund like the S&P 500). The individual who establishes the account (the “authorized individual”) will be able to select among eligible investments.

- Crummey Trust: The trustee or trust investment advisor invests any contributions per the terms of the trust document.

- UTMA: A custodian manages the account on behalf of the minor until they reach the age of majority, including investments.

- 529 Plan: While rules may vary by state, most plans have professional investment managers who invest according to the account owner’s preselected investment option.

Who can control the distributions and to what extent?

When providing for loved ones, especially those who are younger, some families may prefer to have more control over what happens to the funds when it comes to distributions.

- Trump Account: No distributions are permitted until the calendar year the child turns 18.3 At this time, distributions would become subject to most traditional IRA rules, including early withdrawal penalties for distributions made before age 59 ½.4

- Crummey Trust: The beneficiary/beneficiaries has/have a specific window (typically 30 to 60 days) after a gift is deposited to withdraw the funds. If the funds are not withdrawn, they will be distributed according to the trust agreement.

- UTMA: The custodian has control until the beneficiary reaches the age of majority—then the beneficiary has control.

- 529 Plan: Distributions can be made at any time, with those for qualified education expenses being income tax-free. Non-qualified distributions will be taxed on earnings and will be subject to the 10% early withdrawal penalty.

Is there flexibility in case of changed circumstances?

The extent of your ability to make changes, including regaining funds post-transfer or changing a beneficiary, could greatly impact which vehicles you may be comfortable with.

- Trump Account: There is little flexibility, as distributions are severely limited during the growth period. The account may be transferred, but only into another Trump Account for the same individual.

- Crummey Trust: Gifts are irrevocable and beneficiaries cannot be changed without legal action.

- UTMA: Funds transferred are irrevocable and become immediate property of the beneficiary at the time they reach the age of majority. The account cannot be transferred to another individual.

- 529 Plan: The account owner may change the designated beneficiary to another member of the current beneficiary’s family (e.g., spouse, child, or sibling).

What are income, gift, estate, and GST tax considerations?

Taxes can be a major consideration when determining the preferred approach to an annual gifting strategy. Decisions made here could impact your broader wealth planning and should be carefully considered with your tax and legal professionals.

- Trump Account: Funds grow tax-deferred in a TA, with distributions post-growth period taxed according to traditional IRA rules. The IRS released a safe harbor rule for gifts to a Trump Account if certain conditions are met, eliminating the gift tax return filing requirement. Consult a tax professional for more information on gift tax implications.

- Crummey Trust: Income is taxed according to the trust agreement (i.e., whether it is created as a grantor or non-grantor trust). Depending on the beneficiaries, contributions could be covered under the GST annual exclusion.

- UTMA: The minor is the taxpayer when it comes to income tax—often subject to the “kiddie tax”, which effectively imposes tax at the parent’s rate rather than the child’s.

- 529 Plan: Funds grow tax-deferred and withdrawals are income tax-free if used for qualified education expenses. Some states may offer state tax deductions for contributions.

Determining the best use of your annual gift tax exclusion for each loved one ($19,000 for single filers or $38,000 for married couples¹) and whether these vehicles align with your priorities requires careful consideration with a tax professional.

Trump Account FAQs

- Who is eligible for an account? Children who have a Social Security number (SSN) and will not turn 18 before the end of the calendar year are eligible for a Trump Account.

- Who is eligible for the $1,000 federal contribution? Only US citizens with an SSN born between 1/1/25 and 12/31/28 qualify for the federal contribution.

- How do I open a Trump Account for a loved one? Individuals looking to establish a Trump Account for an eligible child must file IRS Form 4547. The Treasury Department will then review and create the account.

- Who can contribute to a Trump Account? Individuals (e.g., parents, grandparents, relatives, friends), governments (e.g., federal, state, local, tribal), employers, and nonprofit entities can contribute to a TA.

- Are there contribution limits? For individuals, the annual contribution limit is $5,000. For employers, the annual limit is $2,500/employee. For government and nonprofit contributions, there is no limit.

Considerations When Gifting

Each of these vehicles comes with benefits and considerations that should be reviewed carefully with legal, tax, and financial advisors. Your gifting strategy and choices could have a far-reaching impact on your and your giftee’s wealth and estate planning. Work with a wealth advisor to understand the potential impacts related to your situation.

1 Annual gift tax exclusion for 2026, to be indexed in future for inflation.

2 There are other types of “present interest trusts,” such as 2503(c) trusts, but this article focuses on Crummey Trusts.

3 Exceptions include: qualified rollover contributions, “qualified ABLE rollover contributions”, distributions of excess contributions, and distributions upon death of the account beneficiary.

4 Subject to certain exceptions.

5 The minor is the taxpayer when it comes to income tax, often subject to the “kiddie tax”, which effectively imposes tax at the parent’s rate rather than the child’s.

6 Some states may charge taxes.

7 This depends on the state. Age of majority is typically 18, 21, or 25.

8 Annual gift tax exclusion for 2026, to be indexed in future for inflation.

This material is provided for informational purposes only and does not constitute an offer or solicitation or a recommendation. It does not take into account any individual’s investment objectives, financial situation, or needs. Goldman Sachs does not provide tax or legal advice; please consult your own advisors regarding your particular circumstances. All investments involve risk, including the possible loss of money invested. Past performance is not indicative of future results. The strategies and vehicles discussed may not be suitable for all investors and involve varying degrees of risk, complexity, and tax treatment. Certain information herein may be based on current legislation or interpretations that are subject to change. Examples are for illustrative purposes only. Goldman Sachs offers a range of services through its affiliates; not all products or services are available in all jurisdictions.

This material is provided for informational purposes only and is not intended to be, and should not be relied upon as, tax, legal, or accounting advice. Goldman Sachs does not provide tax or legal advice unless explicitly agreed upon between clients and Goldman Sachs. Clients should consult their own tax, legal, and financial advisors regarding their particular circumstances before making any decisions.

© 2026 Goldman Sachs. All rights reserved.

Goldman Sachs & Co. LLC is registered with the Securities and Exchange Commission (“SEC”) as both a broker-dealer and an investment adviser and is a member of the Financial Industry Regulatory Authority (“FINRA”) and the Securities Investor Protection Corporation (“SIPC”).